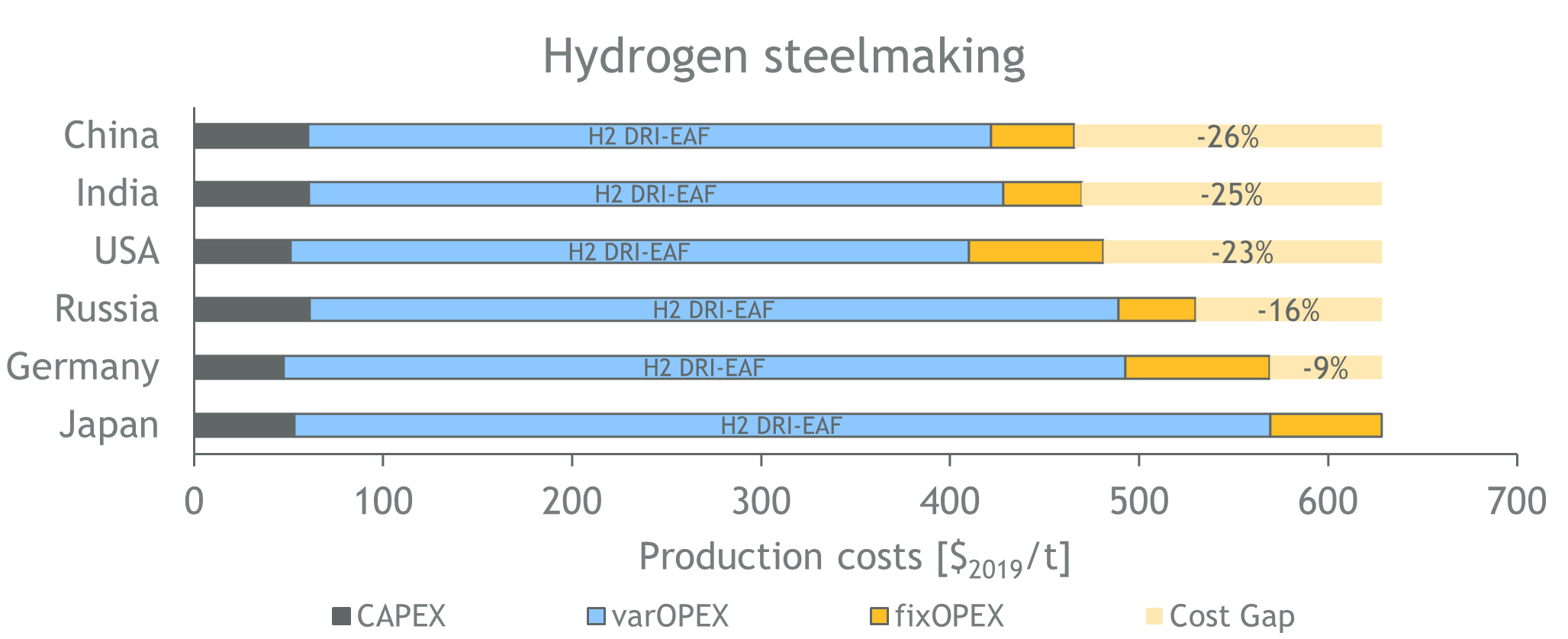

Low-carbon steel production in Germany will remain expensive by international standards. However, the gap to other steel-producing countries (“cost gap”) will narrow if all countries produce low-emission steel. But its coal-based production is emissions-intensive: in 2021, the steel sector was responsible for around 8 percent of global emissions. The aim of COP 26 is to establish nearly zero-emission steel production by 2030.

The Institute of Energy Economics (EWI) at the University of Cologne has now examined low-carbon steel production, the associated costs and the competitiveness of the largest steel-producing countries (China, India, Russia, the United States, Japan and Germany) in an analysis entitled “Low-carbon steel – A global cost comparison”. The analysis was carried out as part of the EWI’s Hydrogen research program and was funded by the Gesellschaft zur Förderung des Energiewirtschaftlichen Instituts an der Universität zu Köln e. V. (Society for the Promotion of the Institute of Energy Economics at the University of Cologne).

In Germany, reducing greenhouse gas emissions from the steel industry means switching from the coal-based “blast furnace route” production process to the lower-emission “direct reduction route,” ideally based on hydrogen. Many climate neutrality studies assume that by 2045 or 2050 primary steel production in Germany will be via the direct reduction route and that less energy- and emissions-intensive secondary steel production (steel recycling) will increase. The challenges here are to maintain the competitiveness of the German steel industry and to prevent carbon leakage, i.e. the relocation of production and thus also emissions to other countries.

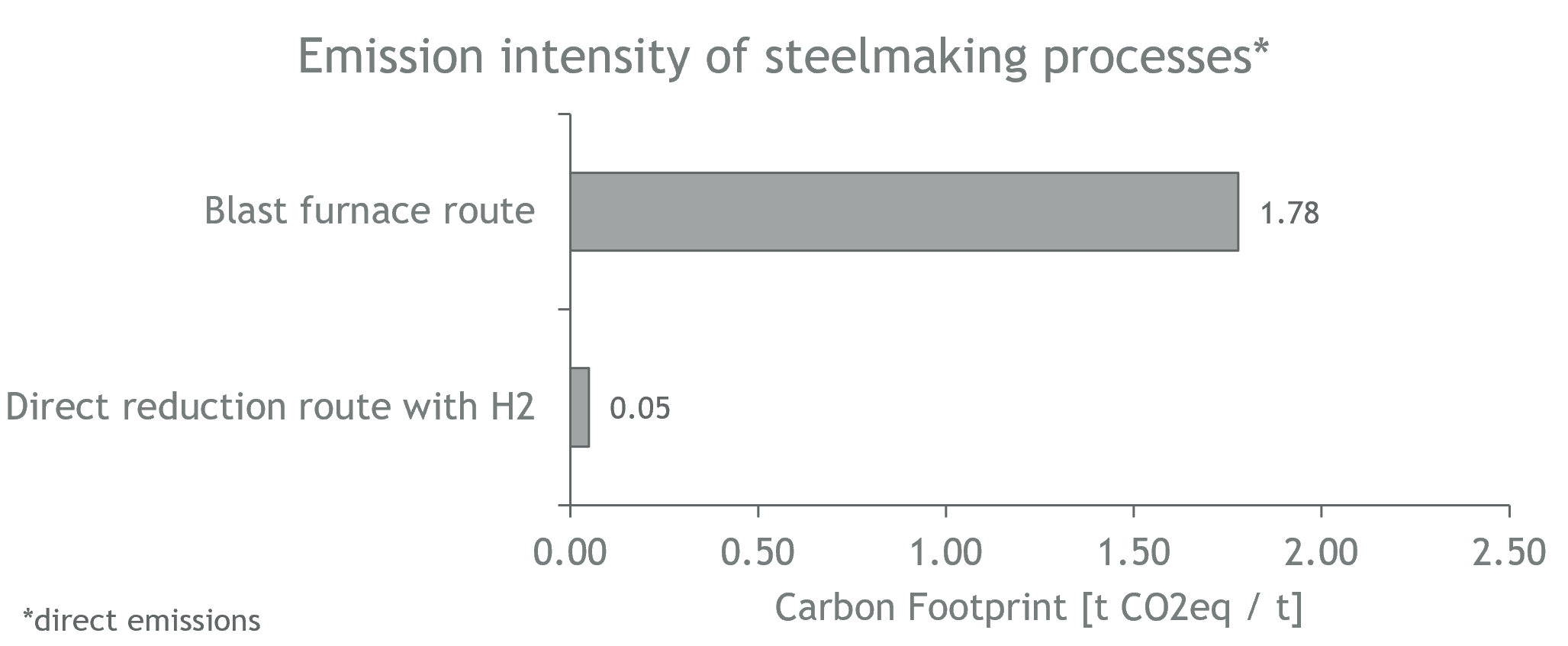

Emissions from the steel industry can be reduced either by using renewable energy and green hydrogen or by Carbon Capture and Storage (CCS). The technology with the lowest intensity of direct CO2 emissions is steel production with hydrogen at 0.05 t CO2 per ton of steel. The technology with the highest emission intensity is the blast furnace route with 1.78 t CO2 per ton of steel.

The study considers three scenarios for a low-carbon steel industry, comparing the production costs of different manufacturing routes and the cost differences (cost gap) between countries:

Due to high energy and labor costs, the production of low-carbon steel is most expensive in Germany and Japan in all scenarios. Hydrogen steel is more expensive to produce in Japan than in Germany. The cost difference between the countries with the highest (Japan) and lowest (China) production costs of low-carbon steel is between 20 and 26 percent in all scenarios. Comparing the possible future cost gap with the historical one shows that the gap tends to decrease. In 2013, the production cost spread between the cheapest and most expensive country was around 45 percent. Nevertheless, all the countries considered are now net exporters, except for the USA.

Commenting on competitiveness, Tobias Sprenger, Senior Research Consultant, says: “In addition to pure production costs, other factors influence competitiveness, such as holding reserve capacities, steel quality, security of supply in the country of manufacture or lower transport costs.”