In the light of the energy transition, the demand for hydrogen storage in Germany could rise to around 40 to 80 TWh, according to a new report by the EWI. In a European comparison, Germany would have the highest number of hydrogen storage facilities, followed by the Netherlands and the UK. The storage facilities would predominantly be converted or newly built salt caverns. In comparison, hydrogen storage facilities have not yet had any relevance for the general energy supply in Germany.

In the report “Hydrogen storage in Germany and Europe: Model-based analysis up to 2050”, a team from the Institute of Energy Economics (EWI) at the University of Cologne examined the future demand for hydrogen storage in the European energy system for several different variations of a scenario. Among other things, the availability of renewable energies, the import quota of green hydrogen and the electricity and hydrogen transport capacities between the European countries were analyzed. The report was commissioned by RWE Gas Storage West.

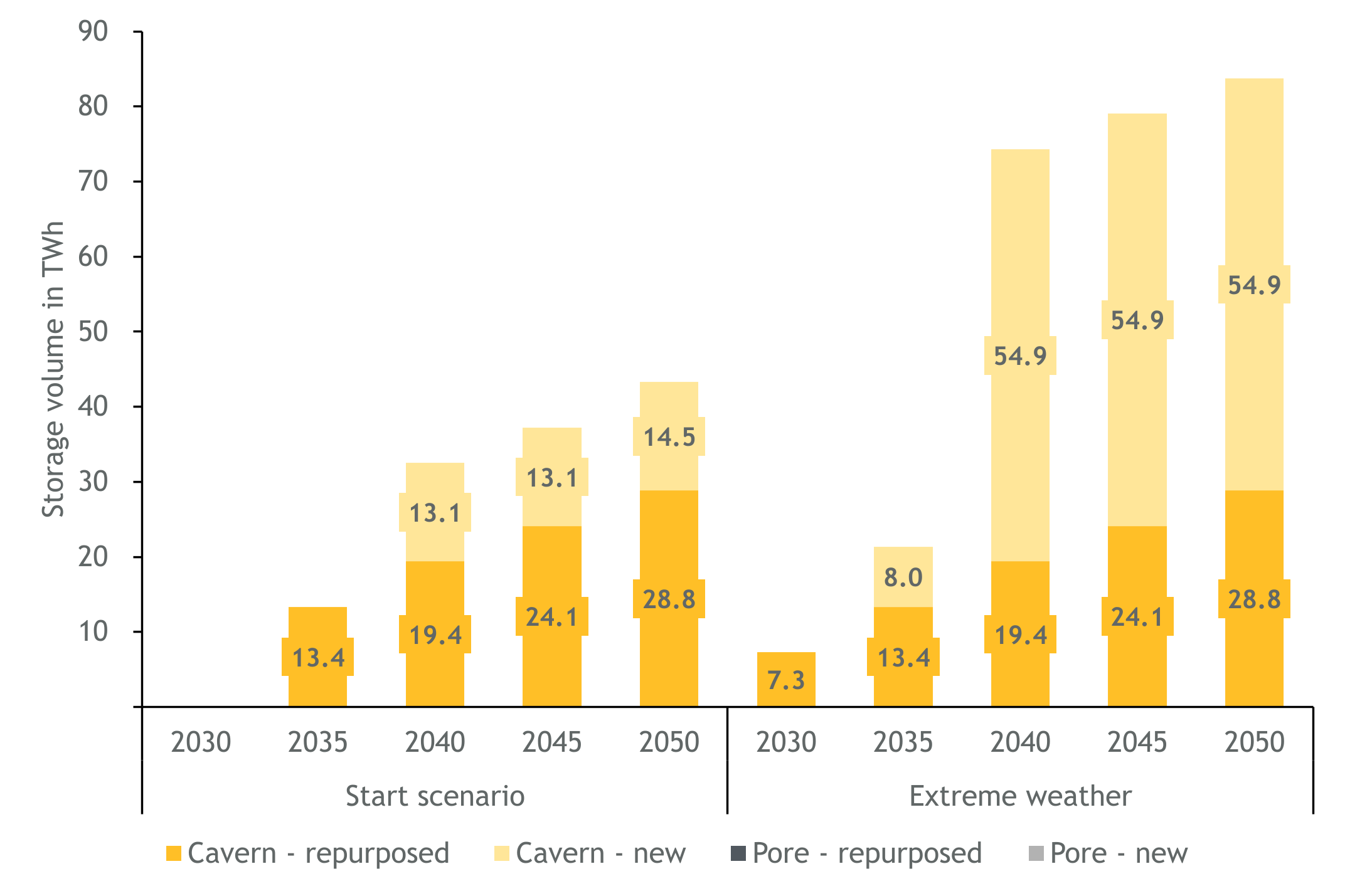

Hydrogen storage supports the security of supply in the hydrogen sector and can be used as electricity storage in a climate-neutral energy system. Of the minimum 40 TWh storage requirement in 2050 in the scenario examined, just under 30 TWh would be accounted for by existing and then converted natural gas storage caverns. The remaining almost 15 TWh would then be new storage capacities. “The conversion of existing natural gas caverns into hydrogen storage facilities could already be necessary by 2030. According to the results of our report, newly built storage capacities could become necessary around 2035,” says Dr. Philip Schnaars, Head of Research Area at the EWI. “With conversion durations of around 5 years, planning would have to begin promptly so that the market ramp-up for hydrogen can succeed.” Around three quarters of the calculated capacities would already be needed by 2040 in the scenario under consideration.

The demand for hydrogen storage depends on several factors, which were examined in a sensitivity analysis as part of the report. The assumed weather conditions have a major influence. For example, the hydrogen storage demand in Germany in the scenario under consideration is approximately twice as high at around 80 TWh if extreme weather periods are examined. If sufficient caverns cannot be rededicated and newly built for storage due to restrictions in the upstream value chains, the analysis shows that storage capacities across Europe would have to be supplemented by more expensive pore storage facilities. By contrast, the overall European storage demand is only slightly influenced by sensitivities such as changes in the import and transportation structures for hydrogen, the costs of expanding and operating storage facilities and the import price for hydrogen.

In the scenario and the sensitivities under consideration, salt caverns would be primarily used to store hydrogen in Germany. These are located in the north, but the main centers of demand for electricity and hydrogen are in southern Germany. This results in a residual load in southern Germany, especially in times of high hydrogen demand from hydrogen power plants, which would have to be covered from the storage facilities in the north. The report shows that the transport capacity of the current draft of the hydrogen core network within Germany may not be sufficient for this in all modeled situations. As a result, pore storage facilities in southern Germany or neighboring countries, additional demand flexibility or an increase in the transport capacity of the hydrogen core network could be necessary for the security of hydrogen supply.

The full report will be published in the course of September.